MONEYME 3Q26 ASX Announcement: Loan book grows to $1.90bn through $325m in originations and positive normalised NPAT achieved for the quarter

MONEYME is pleased to provide its third-quarter trading results for the period ending 31 March 2026.

Trading Highlights

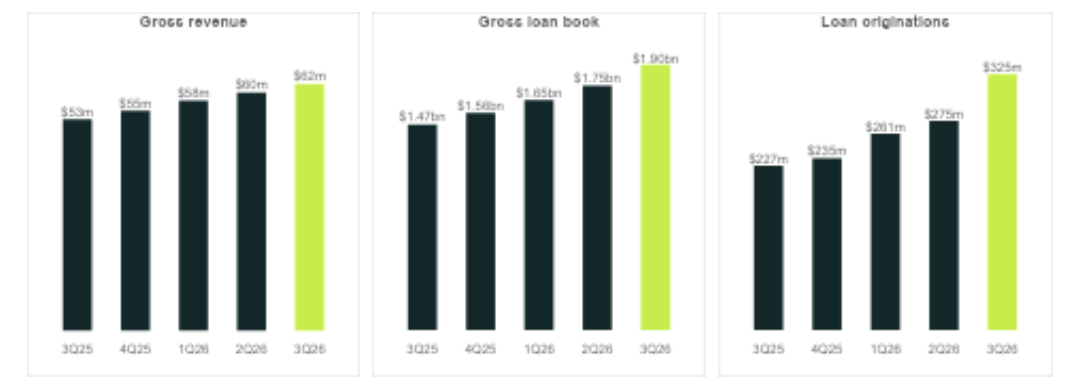

MONEYME delivered strong originations of $325m in 3Q26, up 43% on the prior corresponding period (pcp) and up 18% on 2Q26. Its loan book grew by $150m during the quarter to $1.90bn, up 29% on the pcp, reaching the scale required to achieve Normalised NPAT profitability. Revenue increased to $62m, up 17% on the pcp, while credit performance strengthened, with net credit losses reducing to 2.6%.

MONEYME also launched its new credit card and entered into a strategic white label credit card partnership with Luxury Escapes, supporting continued product diversification and future growth.

Strong growth and credit performance

Loan originations3: $325m for 3Q26 ($227m, 3Q25; $275m, 2Q26), up 43% on the pcp.

Loan book4: $1.90bn as at 31 March ($1.47bn, 3Q25; $1.75bn, 2Q26), up 29% on the pcp.

Gross revenue: $62m for 3Q26 ($53m, 3Q25; $60m, 2Q26), up 17% on the pcp.

Net interest margin (NIM): 6.7% as at 31 March (7.7%, 3Q25; 6.8%, 2Q26), down 0.1 percentage points (pp) on the prior quarter.

Risk-adjusted NIM (RNIM), including corporate interest6: 2.4% for 3Q26 (1.6%, 3Q25; 2.1%, 2Q26), a 0.8 pp improvement on the pcp, reflecting improved credit performance and lower funding costs. New loan originations have an RNIM trending towards circa 3.5% on the current mix of products.

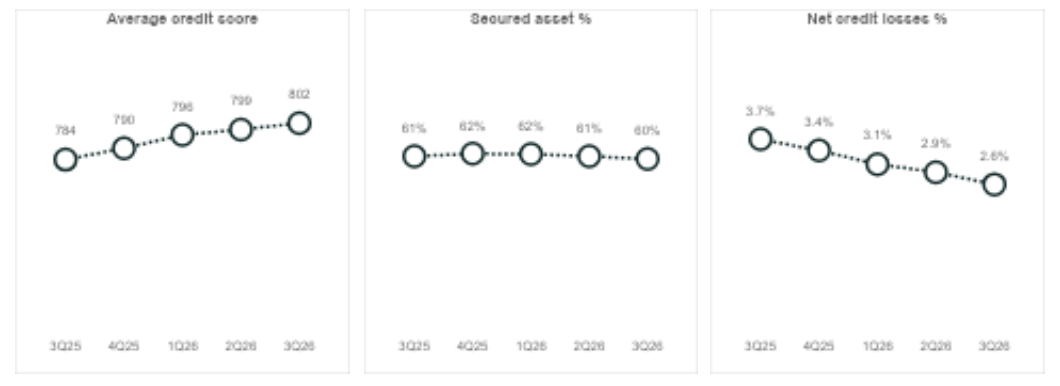

Net credit losses7: 2.6% for 3Q26 (3.7%, 3Q25; 2.9%, 2Q26), a 1.1 pp improvement on the pcp.

90+ arrears: 84bps for 3Q26 (131bps, 3Q25; 96bps, 2Q26), a 47bps improvement on the pcp.

Average credit score8: 802 as at 31 March (within Equifax’s “Very Good” range).

Ratio of secured assets: 60% as at 31 March (61%, 3Q25; 61%, 2Q26).

Increased funding efficiencies

Corporate facility: formalised a 75-basis points reduction in the cost of the facility.

Cost of funds: funding cost improvements realised as a result of 1H26 capital markets transactions and the first drawdown of the new credit card warehouse facility, with its significantly lower funding costs and more capital-efficient structure.

Innovation and product developments

New credit card launch: MONEYME’s Cashback Rewards Credit Card successfully launched in 3Q26, with recognition from Finder as the number one cashback credit card. Customer adoption has been strong.

Luxury Escapes co-brand credit card: the Luxury Escapes white-label credit card partnership was signed with an expected launch in 4Q26.

Clayton Howes, MONEYME’s Managing Director and CEO, said:

“The third quarter marked a step-change in performance, with originations increasing by $50m quarter-on-quarter and the loan book reaching $1.90bn. This represents an inflection point, delivering a positive Normalised NPAT in the quarter, with revenue growth outpacing costs and driving operating leverage.

Despite interest rate and inflation pressures, our credit performance remains strong with loss rates declining as we continue to focus on secured vehicle finance and high credit quality segments. This, alongside a predominantly variable interest rate loan book enables us to absorb these market pressures, maintain risk-adjusted NIM, and price effectively for capital preservation.

Funding remains a key strength, with a robust corporate facility and strategic partnership with iPartners delivering favourable terms, including a 75-basis point reduction in funding costs that further supports growth and margin outcomes.

We continue to capture market share in under-served segments through fast, innovative and well-priced products and outstanding customer service. At the same time, our multi-product strategy is gaining traction, with momentum building in credit cards. The launch of our Cashback Rewards Credit Card and upcoming white-label partnership with Luxury Escapes will expand access to millions of potential customers. While credit card growth may have a near-term impact on profitability, it is expected to deliver meaningful margin expansion as the portfolio scales.”

Illustration of target scale and annualised profitability outcomes

Loan book and revenue growth outpacing costs to deliver operating leverage

MONEYME’s strategy of balancing product mix and credit quality continues to deliver improving returns, with lower credit losses, reduced funding costs, and an increasing RNIM, positioning the business at the inflection point for delivering positive Normalised NPAT.

Higher quality loan book delivers lower credit losses

Strategy and outlook

MONEYME remains on track to deliver on its FY26 strategic priorities, supported by strong growth in originations, continued improvement in credit performance and execution across its product roadmap. AI and automation are increasingly embedded across product engineering, credit decisioning, marketing and operations. These investments are enhancing speed, improving decision accuracy and driving significant operating efficiencies across the company.

MONEYME reached a Normalised NPAT profitability inflection point in 3Q26 with its $1.90bn loan book. Its efficient operating cost model, strong credit performance and healthy risk adjusted NIM settings, provide the platform for increased operating leverage as the loan book continues to scale, subject to prevailing market conditions.

Credit cards and white-label partnerships are expected to contribute to the returns profile of the business in time, when the credit card loan book reaches scale.

Authorised by the Disclosure Committee.

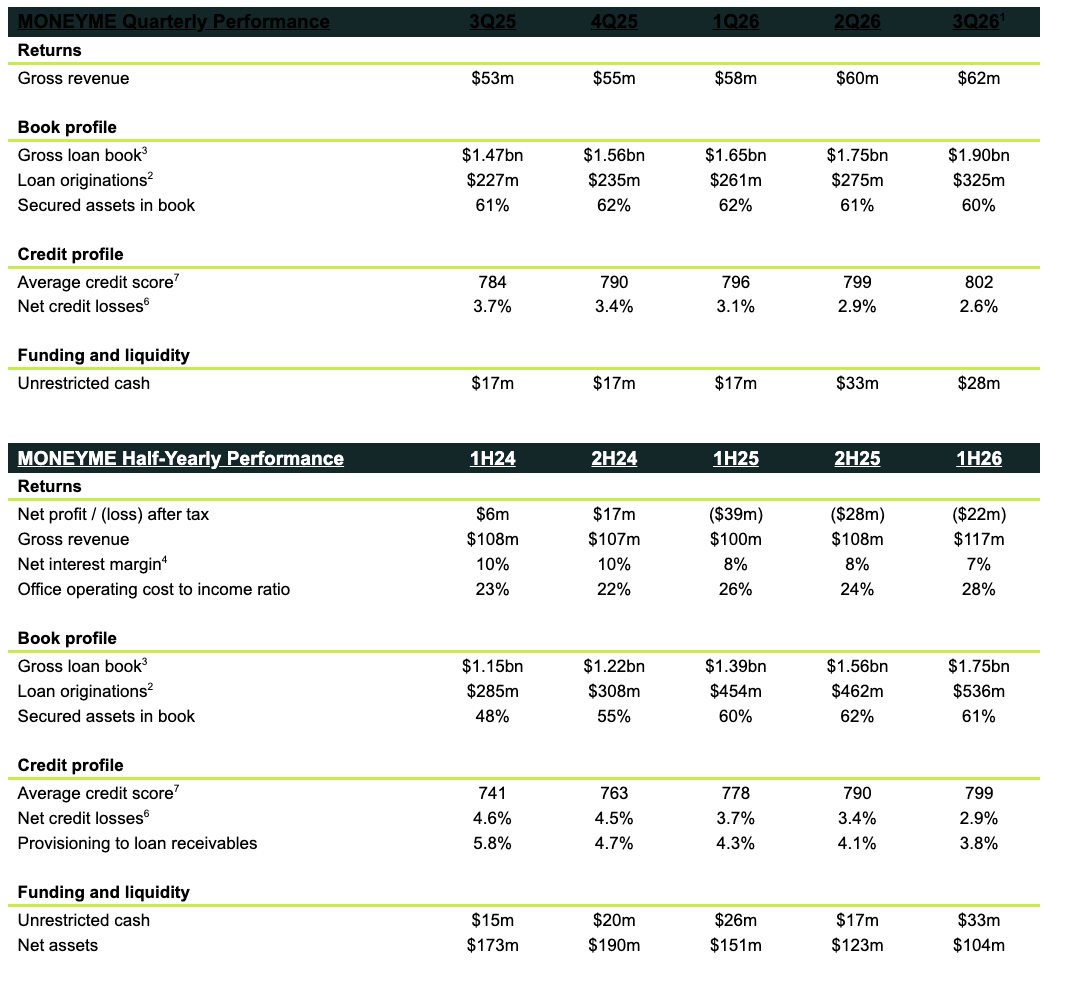

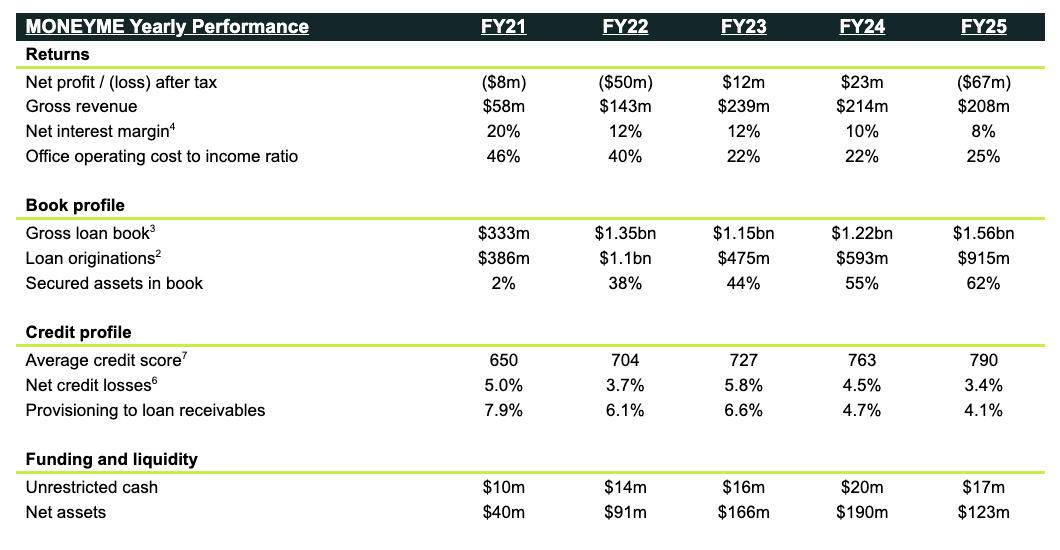

Historical performance measures1

About MONEYME

MONEYME (ASX: MME) is a fintech lender challenging the banks on speed, service and products for Australians who expect better. Its proprietary technology platform enables real-time, AI-powered credit decisioning in minutes, unlocking flexible lending solutions across personal loans, auto finance, credit cards and financial management tools. As a purpose-driven Certified B Corporation™, social and environmental responsibility, strong governance and customer-first innovation are embedded across its operations.